Original source: Kairos Research

Original compilation: Luffy, Foresight News

summary

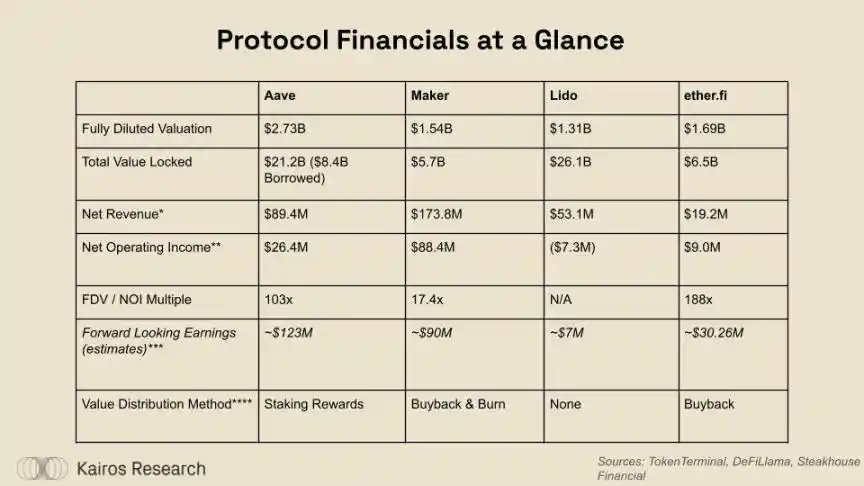

This report aims to explore some of the most influential DeFi protocols from a financial perspective, including a brief technical overview of each protocol and an in-depth study of their revenue, payouts, and token economics. Given the unavailability of regularly audited financial statements, we used on-chain data, open source reporting, governance forums, and conversations with project teams to estimate Aave, Maker (Sky), Lido, and ether.fi. The table below presents some of the key conclusions we reached throughout the study, giving readers a comprehensive understanding of the current status of each protocol. While the P/E ratio is a common way to determine whether a project is overvalued or undervalued, key factors such as dilution, new product lines, and future earnings potential can tell a fuller picture.

Notes: 1. DAI savings interest rate is included in the cost of income, but not in Aave’s security module; 2. Ether.fi token incentives are not included because they are in the form of airdrops; 3. This is a new product through a new product ( The rough results of growth rates, interest rates, ETH price appreciation and margin estimates for GHO, Cash, etc., should not be considered investment advice; 4. Aave is currently looking to improve token economics, including AAVE repurchases and distributions

From the analysis it can be concluded that after years of liquidity guidance and moat building, we are witnessing some protocols moving to a sustainable profitability stage. For example, Aave has reached a turning point, achieving profitability for several months and is rapidly developing a new, higher-margin loan product through GHO. ether.fi is still in its infancy, but has accumulated over $6 billion in total locked value, ensuring it ranks among the top five DeFi protocols in terms of scale. The liquidity rehypothecation leader has also learned from some of Lido’s shortcomings and launched a number of other ancillary products with higher interest rates to make the most of its billions of dollars in deposits.

Problem statement and definition

Since the rise of DeFi in 2020, on-chain data and analytical methodology tools have steadily improved, with companies such as Dune, Nansen, DefiLlama, TokenTerminal, and Steakhouse Financial playing key roles in creating real-time dashboards on the status of crypto protocols. At Kairos Research, we believe that an important way to cultivate credibility within the industry is to drive standardization across protocols and DAOs to demonstrate financial performance, health, and sustainability. In cryptocurrencies, profitability is often overlooked, but value creation is the only way to sustainably align every actor within the protocol (users, developers, governance, and community).

Here are some terms we will use throughout the study to try to standardize the approximate cost of each protocol.

· Total revenue/fees: includes all revenue generated by the protocol, belonging to the users of the protocol and the protocol itself.

· Commission ratio: The percentage of fees charged by the protocol to users.

· Net revenue: The remaining protocol revenue after paying fees to protocol users and deducting revenue costs.

· Operating Expenses: Various protocol expenses including salaries, contractors, legal and accounting, audits, gas costs, grants and possible token incentives, etc.

· Net Operating Income: The net dollar amount after subtracting all costs incurred by the protocol and token holders (including token incentives related to operating the protocol).

· Adjusted earnings: One-time charges are added back to earnings to more accurately predict future earnings, minus known future costs that are not currently expressed through earnings.

Protocol Overview

We will provide a detailed analysis of the core products offered by each of the highlighted protocols in this report, which span the most mature protocols across a range of crypto niches.

Ghost

Aave is a “decentralized, non-custodial liquidity protocol in which users can participate as providers, borrowers or liquidators.” Providers deposit crypto assets to earn loan proceeds and gain lending capabilities themselves, so that They can then leverage or hedge their deposited positions. Borrowers are either over-collateralized users looking for leverage and hedging, or they are taking advantage of atomic flash loans. Borrowers must pay a fixed or floating interest rate on the specific asset they borrow. Aave’s protocol fee is the total amount of interest paid on open (unrealized), closed or liquidated positions, and is then split between lenders/vendors (90%) and the Aave DAO treasury (10%). In addition, when a position exceeds its specified loan-to-value ratio limit, Aave will allow the “liquidator” to liquidate the position. Each asset has its own liquidation penalty, which is then divided between the liquidator (90%) and the Aave DAO treasury (10%). Aave’s new offering, GHO, is an over-collateralized, cryptocurrency-backed stablecoin. The introduction of GHO eliminates the need for Aave to rely on third-party stablecoin providers when providing loans, giving them greater flexibility in interest rates. Additionally, GHO cuts out the middleman and allows Aave to receive full borrowing interest on outstanding GHO loans.

Aave transparently displays all the DAO’s income, expenses and other data through the Tokenlogic dashboard. We took the “fiscal revenue” data from August 1 to September 12 and annualized the numbers, resulting in net revenue of $89.4 million. To arrive at the total revenue figure, we relied on TokenTerminal’s income statement data to estimate profit margins. Our forecast for 2025 is primarily based on assumptions, including that an upward trend in crypto asset prices will lead to increased borrowing capacity. Additionally, Aave’s net profit margin increases in our model due to the potential replacement of third-party stablecoins by GHO, as well as improvements to the protocol’s security module, which will be explained further below.

Cryptocurrency’s leading lending market is on track to see its first profitable year in 2024. Several signs point to Aave’s profit potential: supplier incentives have dried up and active lending continues to trend upward, with active borrowing exceeding $6 billion. Aave is clearly a huge beneficiary of the liquid staking and re-staking market, as users deposit LST/LRT, lend out ETH, exchange ETH for liquid staking tokens, and then repeat the same process again. This cycle allows Aave users to earn a net interest margin (APY associated with LST/LRT deposits – Aave borrowing interest) without taking on huge price risk. As of September 12, 2024, ETH is Aave’s largest outstanding loaned asset, with over $2.7 billion in active loans across all chains. We believe that this trend driven by the concept of proof of stake + re-staking has changed the landscape of the on-chain lending market, greatly increasing the utilization of protocols such as Aave in a sustainable way. Before re-staking-driven circular lending became popular, these lending markets were dominated by leveraged users, who tended to only borrow stablecoins.

The launch of GHO creates a new, higher-margin lending product for Aave. It is a synthetic stablecoin where borrowing fees are not paid to the provider. It also allows the DAO to offer interest rates slightly below the market, thereby driving demand for borrowing. From a financial perspective, GHO is undoubtedly one of the most important parts of Aave to focus on in the future, as the product has:

· High upfront costs (technology, risk and liquidity)

· The cost of audits, development work, and liquidity incentives will slowly decrease over the next few years

· Relatively large upside potential

· The outstanding GHO supply is $141 million, accounting for only 2.35% of Aave’s total outstanding loans and 2.7% of the DAI supply

· Currently, non-GHO stablecoins (USDC, USDT, DAI) lent on Aave are close to $3 billion

· A lending market with higher profit margins than Aave

· While there are other costs to consider when issuing a stablecoin, it should be cheaper than having to pay a third-party stablecoin provider

· MakerDAO’s net income margin is 57%, while Aave’s margin is 16.31%

The fully diluted valuation (FDV) of AAVE, the native token of the Aave protocol, is $2.7 billion, which is equivalent to about 103 times its annual earnings (estimated $26.4 million), but we believe this value will change in the coming months. As discussed above, favorable market conditions can increase borrowing capacity, stimulate new demand for leverage, and may be accompanied by liquidation proceeds. Finally, even if GHO’s market share growth is simply the result of cannibalizing Aave’s traditional lending market, it should have a direct positive impact on margins.

MakerDAO

MakerDAO (renamed Sky) is a decentralized organization that supports the issuance of stablecoins (DAI) by mortgaging various cryptocurrencies and real-world assets, so that users can both utilize their own assets and allow the crypto economy to gain access to Centralized stable value storage. Maker’s protocol fee is the “stability fee”, which is composed of the interest paid by the borrower and the income generated by the agreement allocated to the income-generating assets. These protocol fees are distributed between MakerDAO and depositors who deposit DAI into the DAI Savings Rate (DSR) contract. Like Aave, MakerDAO also charges a liquidation fee. When a user’s position falls below the necessary collateral value, the asset will be liquidated through an auction process.

MakerDAO has thrived over the past few years, aided by liquidations during 2021’s speculative volatility. But as global interest rates rise, MakerDAO has also created a more sustainable, lower-risk business line. The introduction of new collateral assets, such as US Treasury bonds, allows Maker to increase asset efficiency and generate returns above standard DAI lending rates. When exploring DAO payouts, we clearly understand the following:

· DAI is deeply rooted in the entire crypto ecosystem (CEX, DeFi), which allows Maker to avoid investing millions of dollars in liquidity incentives.

· The DAO does a great job of prioritizing sustainability

Throughout 2024, Maker is expected to generate approximately $88.4 million in net agreement revenue. MKR is valued at $1.6 billion, which is just 18 times net revenue. In 2023, the DAO voted to modify the protocol’s token economics to return a portion of the proceeds to MKR holders. As DAI continues to accumulate borrowing rates (stability fees) into the protocol, Maker accumulates a system surplus, which they aim to keep at around $50 million. Maker introduces a smart destruction engine and uses surplus funds to repurchase MKR in the market. According to Maker Burn, 11% of the MKR supply has been bought back and used for burning, the protocol’s own liquidity, or vault construction.

Lido

Lido is the largest liquidity staking service provider on Ethereum. When users stake ETH through Lido, they receive “liquid staking tokens” so that they can avoid the queuing period to cancel their pledge and the opportunity cost of not being able to use their staked ETH in DeFi. Lido’s protocol fee is the ETH revenue paid by the verification network, distributed among stakers (90%), node operators (5%), and the Lido DAO treasury (5%).

Lido is an interesting case study of DeFi protocols. As of September 10, 2024, they had 9.67 million ETH staked through their protocol, accounting for approximately 8% of the entire ETH supply and more than 19% of the staking market share, with a total locked value of $22 billion. However, Lido still lacks profitability. What changes can be made to enable Lido to generate cash flow in the short term?

In the past two years alone, Lido has made huge strides in cutting costs. Liquidity incentives are very important in bootstrapping stETH, and advanced users will naturally gravitate towards LST as it has the best liquidity in the entire ecosystem. We believe that with stETH having an impressive moat, Lido DAO will be able to further reduce liquidity incentives. Even with cost cuts, $7 million in profits may not be enough to justify LDO’s $1 billion-plus FDV.

In the coming years, Lido will have to look to expand earnings or cut costs to reach its valuation. We see several potential avenues for growth for Lido, either as the ETH network-wide pledge rate continues to rise from 28.3%, or as Lido works to expand outside of the Ethereum ecosystem. We believe that over a long enough time horizon, the former is very likely to be achieved. In comparison, Solana’s staking ratio is 65.5%, Sui’s 79.5%, Avalanche’s 49.2%, and Cosmos Hub’s 61%. By doubling the amount of ETH staked and maintaining its market share, Lido will be able to generate an additional $50 million in net revenue. This assumption is too simplistic and does not take into account that ETH issuance rewards will be compressed as the staking ratio increases. While Lido’s current market share gains are also possible, we see Ethereum’s social consensus casting serious doubts on Lido’s dominance in 2023, marking the peak of its growth spurt.

ether.fi

Like Lido, ether.fi is a decentralized, non-custodial staking and re-staking platform that issues liquid receipt tokens for users’ deposits. ether.fi’s protocol fees include ETH staking earnings and active verification service revenue, which are used to provide economic security through the Eigenlayer ecosystem. ETH staking rewards are distributed to stakers (90%), node operators (5%) and ether.fi DAO (5%), and then Eigenlayer/re-staking rewards are distributed to stakers (80%), node operators (10 %) and ether.fi DAO (10%). ether.fi has a number of other ancillary products that can generate significant revenue, including “Liquid,” which is a library of re-staking and DeFi strategies designed to maximize returns for depositors. Liquid charges a 1-2% administrative fee on all deposits, which will be rolled into the ether.fi protocol. Additionally, ether.fi recently launched a Cash debit/credit card product that allows users to make real-life payments using re-pledged ETH.

As of September 2024, ether.fi is the undisputed market leader in liquidity rehypothecation, with a TVL of $6.5 billion in rehypothecation and yield products. We tried to model the potential protocol revenue for each of its products using the following assumptions in the financial statements above:

· Assuming ether.fi’s current staking volume remains unchanged for the remainder of the year, the average TVL pledged in 2024 will be approximately $4 billion

· The average ETH staking yield will drop by about 3.75% this year

· EIGEN’s pre-listing FDV is approximately US$5.5 billion, and the issuance plan for re-staking rewards is 1.66% in 2024 and 2.34% in 2025, which means that ether.fi’s direct income from EIGEN is: approximately US$38.6 million in 2024 and 2025 Approximately US$54.4 million annually

· By studying EigenDA, Omni and other AVS reward programs, we estimate that Eigenlayer restakers will be paid a total of approximately $35-45 million in rewards, with an annual yield of 0.4%

Cash is the hardest revenue stream to model because it has just launched and there is a lack of transparent precedent in the entire space. We and the ether.fi team will make our best estimate for 2025 based on booking demand and the cost of revenue for the major credit card providers, which we will be watching closely over the coming year.

While we understand that ETHFI token incentives are a cost of the protocol, we decided to leave them at the bottom of the financial statements for the following reasons: These fees are heavily invested upfront due to airdrops and liquidity bootstrapping, and these fees are not necessary for business development cost, and we believe that the EIGEN + AVS rewards are enough to offset the cost of ETHFI incentives. Given that withdrawals have been enabled for some time and ether.fi has seen significant net outflows, we believe the protocol is closer to achieving long-term sustainable TVL targets.

Token value accumulation and scoring system

Beyond simply assessing the profitability of these protocols, it’s also worth exploring where each protocol’s revenue ultimately flows. Regulatory uncertainty has been a driver of the creation of numerous revenue distribution mechanisms. Dividends to token stakers, buybacks, token burnings, accumulation within treasuries, and many other unique methods have been employed in an attempt to keep token holders involved in protocol development and incentivized to participate in governance. In an industry where token holder rights do not equal shareholder rights, market participants must thoroughly understand the role their tokens play in the protocol. We are not lawyers and do not take any position on the legality of any allocation method, simply exploring how the market will react to each method.

Stablecoin/ETH Dividends:

Pros: Measurable benefits, higher quality returns

Disadvantages: taxable events, gas consumption, etc.

Token buyback:

Advantages: tax exemption, continued purchasing power, growing funds

Disadvantages: prone to slippage and front-running, no guarantee of returns for holders, funds concentrated on native tokens

Buyback and destruction:

Pros: Same as above, increased earnings per token

Disadvantages: Same as above + no capital growth

Treasury accumulation:

Advantages: Increase the operating space of the protocol, achieve diversification of funds, and still be controlled by DAO participants

Disadvantages: No direct benefit to token holders

Tokenomics is clearly an art, not a science, and it’s hard to know who would benefit more from distributing earnings to token holders than from reinvesting them. For the sake of simplicity, in a hypothetical world where the protocol has maximized growth, having tokens that redistribute earnings will increase the IRR for holders and eliminate each time some form of payout is received risk. Below we explore the design and potential value accumulation of ETHFI and AAVE, both of which are currently undergoing token economics improvements.

Looking to the future

Ghost

Currently, the supply of GHO is 142 million, the weighted average borrowing rate of GHO is 4.62%, the weighted average stkGHO incentive payout is 4.52%, of which 77.38% of the total GHO supply is pledged in the security module. Therefore, Aave earns 10 basis points on $110 million worth of GHO and 4.62% on $32 million uncollateralized. Taking into account global interest rate trends and stkAAVE discounts, there is certainly room for GHO borrowing rates to drop below 4.62%, so we have also increased our forecasts for the impact of GHO to 4% and 3.5% respectively. Aave should have many opportunities to grow GHO in the coming years, and the chart below predicts how the path to $1 billion in outstanding GHO loans will impact protocol earnings.

While Aave has growth potential, Marc Zeller also proposed a temperature check within Aave’s governance forum to improve the protocol’s payouts as well as its native token AAVE. The improvements come on the premise that Aave is quickly becoming a profitable protocol but is currently overpaying for imperfect security modules. As of July 25, Aave had $424 million in its security module, consisting primarily of stkAAVE and stkGHO, both of which are imperfect assets that cannot cover bad debts caused by slippage and decoupling risks. Additionally, through token issuance, the protocol is incentivizing secondary liquidity for AAVE so that slippage can be minimized if stkAAVE must be used to cover bad debt.

This concept could completely change if the DAO votes to use aTokens like awETH and aUSDC as security modules while isolating stkGHO to only pay back GHO debt. stkGHO never needs to be sold to cover bad debts, just confiscated and burned. The above-mentioned aTokens are extremely liquid and constitute the majority of the protocol’s debt. If the collateral is insufficient, these pledged aTokens may be confiscated and burned to cover bad debts. The goal of the proposal is to reduce spending on security modules and liquidity incentives. Zeller further explains stkAAVE’s role under the new scheme in the image below.

If the proposal passes, it should have a favorable impact on the AAVE token as it will have a more stable demand, while also allowing holders to receive rewards without the risk of stkAAVE being confiscated to cover bad debts. We are unsure of the tax implications of the staking contract, but it greatly benefits long-term holders of AAVE through continued purchasing power and redistribution of tokens to stakers.

ether.fi

Given ether.fi’s success in quickly creating a sustainable business model, establishing multiple monetization initiatives is attractive. For example, the protocol’s development team and DAO acted very quickly, proposing that the company use 25% -50% of the revenue generated by Restaking & Liquid products to buy back ETHFI for liquidity supply and capital reserves. However, using 2024 earnings numbers to calculate a fair valuation may be futile and complicated given the lack of AVS incentives, the substantial startup costs up front, and the fact that much of its product suite is brand new.

The ETHFI token has an FDV of $1.34 billion and is expected to be slightly profitable this year (excluding liquidity incentives), making it very similar to Lido’s LDO. Of course ether.fi must stand the test of time, the protocol has the potential to monetize faster than Lido and has a higher ceiling given the continued success of the broader product. Below is a conservative analysis of how AVS rewards will contribute to protocol revenue. AVS reward yield is the reward that re-stakers receive from AVS payouts only.

As seen on Lido, liquidity staking/re-staking is a highly competitive industry with relatively thin margins. ether.fi has fully recognized this limitation and is exploring the creation of a wider range of revenue auxiliary products while occupying market share. Here’s why we think these other products fit their broader rehypothecation and yield generation thesis.

· Liquid: We firmly believe that LRT power users are familiar with the DeFi legos and want to maximize their returns, thus attracting them to products that can automate their DeFi strategies. Once AVS rewards truly “go live,” dozens of risk/reward strategies and a new form of native income will emerge in the crypto economy.

· Cash: Similar to LST, LRT is a superior form of collateral than ordinary ETH, and they have sufficient liquidity. Users can either use Liquid Rehypothecation as a profitable checking account or borrow assets for daily expenses at virtually zero cost.